More resilient to market shocks than other industries

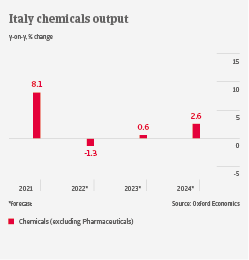

After a robust rebound in 2021, chemicals output and sales have slowed sharply since H1 of 2022. Exports as a main driver of growth have plummeted, as demand from main European markets (France, Germany) has decreased. Domestic demand from automotive and textiles remains modest. Sales to construction are also slowing down, affecting the paints and coating segment. High inflationary pressures impact household consumption of soaps and detergents.

Due to the currently very high energy and feedstock prices, Italian chemicals manufacturers face competitive headwind from overseas peers, while at the same time demand from main-end markets is decreasing. Additionally, there are supply chain issues with virgin naphtha, one of the main raw materials needed by the Italian chemicals industry. Rising prices for commodities and gas have caused some chemicals manufacturers to stop production and to apply for furlough schemes. The scope and scale of public support to shield businesses from high energy prices remain to be seen.

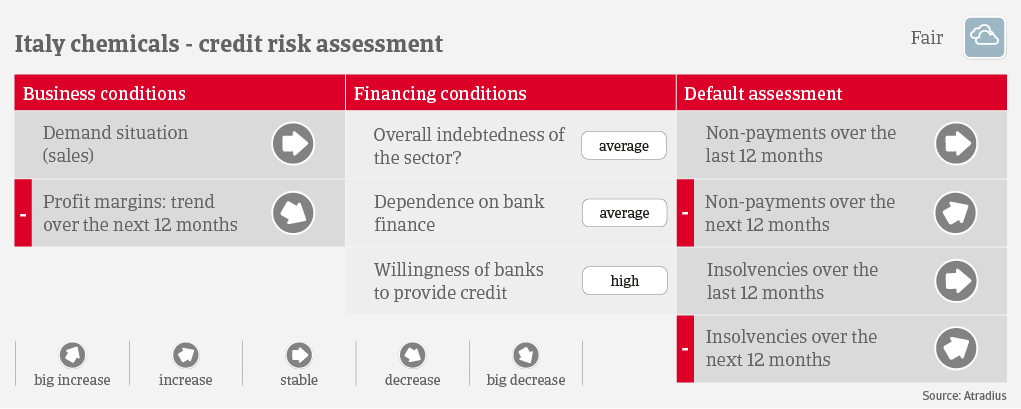

Despite deteriorating margins, Italian chemical manufacturers remain well capitalized and not overly dependent on external financing. This makes the industry more resilient to market shocks compared to other sectors.

Due to very high energy costs, we expect payment delays to increase in the coming 12 months. According to the latest Atradius Payment Practices Barometer, Days Sales Outstanding (DSO) average more than 100 days, and there is concern among businesses about deteriorating DSO in the coming months. We also expect more insolvencies in this period, although from a very low level. In case of a serious shortage of gas over a longer period, or gas rationing, the insolvency risk would sharply increase, particularly for smaller chemical producers and traders.

Despite the current major challenges, we assess the credit risk situation of the Italian chemicals sector still as “Fair”, due to its financial resilience and low default rate. The basic and specialties segments continue to perform well, while we perceive higher credit risk in the agrochemicals segment. This subsector suffers severely from a shortage of raw materials, which previously mainly came from Ukraine and Russia, while payment collection time is historically long.

Related documents

2.03MB PDF