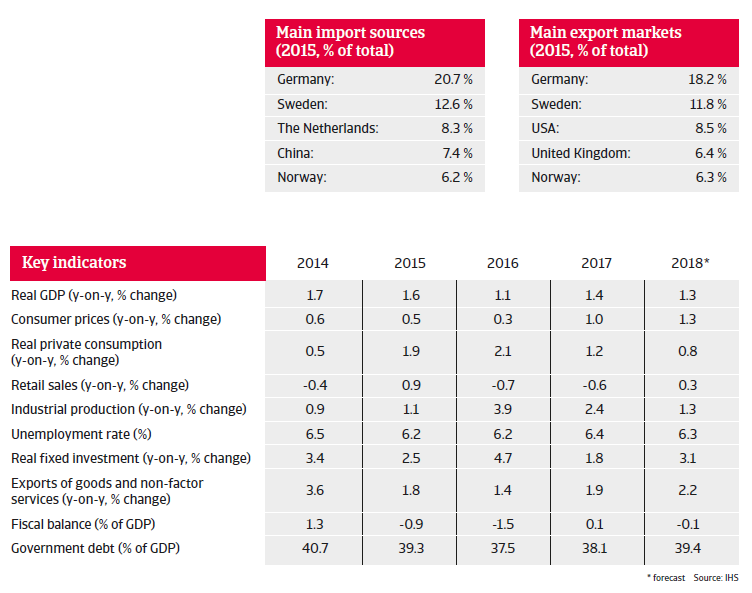

The Danish economy has regained some of its international competitiveness due to structural reforms that addressed the issue of high labour costs.

The insolvency environment

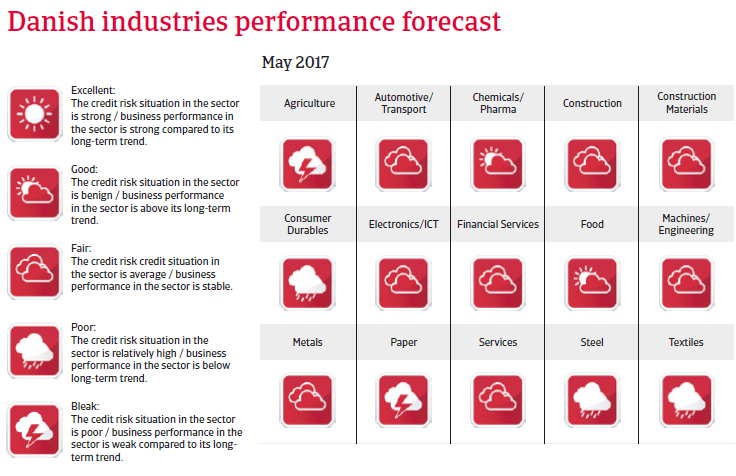

Sharp, but exceptional insolvency increase in 2016

Danish business insolvencies increased sharply in 2016 due to the introduction of a new form of company in official statistics and the clearing of a backlog of insolvencies. As such, it is difficult to provide an accurate forecast on real businesses and insolvency development in 2017. It is expected that business failures will decline by about 20% this year, an adjustment from exceptionally high levels in 2016.

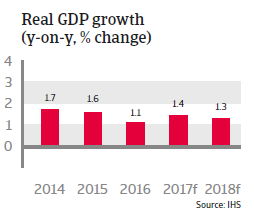

Economic situation

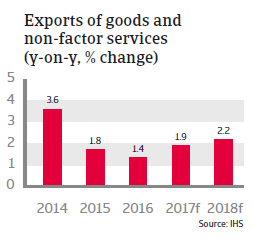

Exports to pick up