Solid economic growth is expected to continue in 2017 and 2018, but the Brexit decision will most probably affect Dutch industries in the mid-term.

The insolvency environment

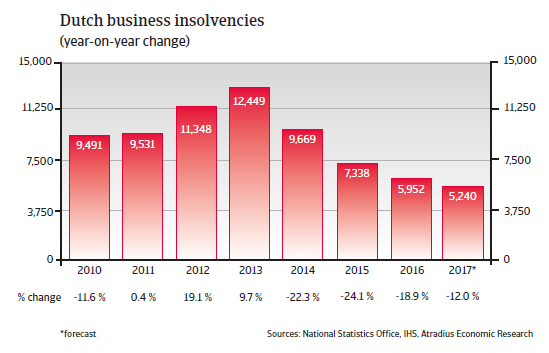

Corporate insolvency decrease expected to slow down in 2017

The economic slowdown in 2012 and 2013 triggered sharp increases in business insolvencies. Due to the economic rebound since 2014 business failures started to decrease again, declining 18.9% to 5,952 cases in 2016, (including sole proprietorships). The positive trend is expected to continue in 2017.

Economic situation

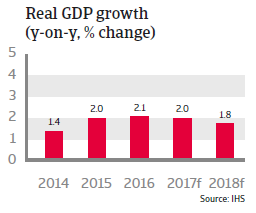

Solid growth to continue in 2017 and 2018

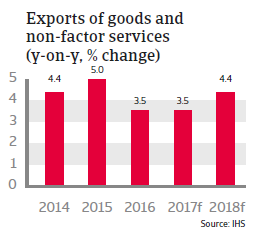

The Dutch economy has gained momentum in 2015 and 2016, and is forecast to continue to grow in 2017 and 2018 by about 2% annually. All spending categories are expected to contribute to the economic expansion. Private consumption benefits from decreasing unemployment (which has decreased substantially over the past three years), an increase in disposable income and a 15% rebound of house prices since 2013. At the same time, inflation will increase to 1.6% in 2017 due to higher energy prices. Dutch exports continue to benefit from higher global demand and the depreciation of the euro. Due to past austerity measures and the on-going economic growth, the budget deficit is expected to remain small or even turn into a surplus in 2017 and 2018.

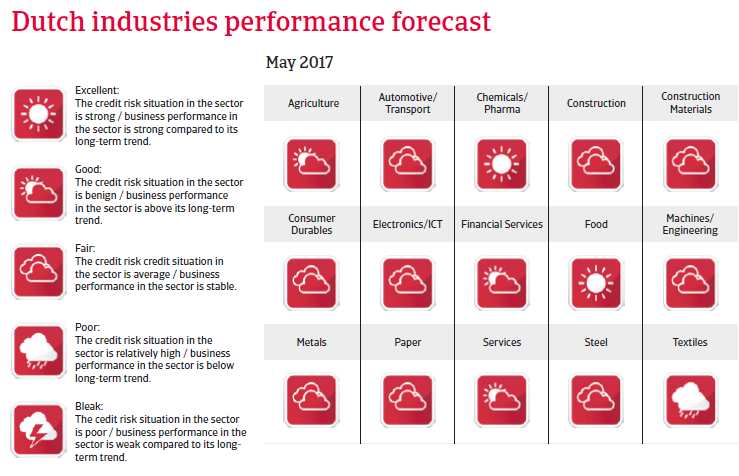

The Brexit decision will most probably affect Dutch industries in the mid-term, due to close trade and investment ties between the Netherlands and the UK. The sectors to be mainly affected are chemicals, electronics, food and metals.