Very long payment duration remains an issue for the industry

After a 6.6% contraction in 2020, a rebound of about 12% is forecast for Italian construction output in 2021, and 0.5% growth in 2022. Residential building and civil engineering are driving the recovery. The Next Generation EU fund will make large investments in projects with a sustainability aspect. Out of the fund EUR 224 billion are assigned to Italy in the 2021-2026 period, with about 50% earmarked for construction projects.

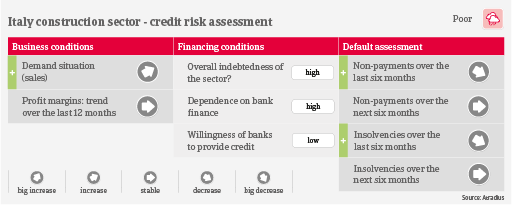

The sharp increase in commodity prices will negatively affect businesses' profitability in the coming months. However, it is expected that builders will increasingly be able to pass on higher prices for construction materials to end-customers. While construction companies are highly dependent on loans, banks remain generally unwilling to provide credit to the industry, due to high levels of payment delays and defaults seen over the past couple of years. At least lending conditions have eased somewhat recently, mainly through state guarantees for bank loans.

Payments in the Italian construction industry take a whopping 200 - 250 days on average. SMEs in particular suffer from the bad payment behaviour of public bodies. In the years before the coronavirus outbreak, the Italian construction sector stood out with a persistently high level of non-payments and high numbers of business failures, including the insolvencies of several larger players. Due to pandemic-related stimulus measures both non-payment delays and insolvencies decreased in 2020 and in H1 of 2021. No substantial increase is expected in the coming months..

Despite the surge in demand and the benign short-term insolvency outlook, our industry assessment remains “Poor” for the time being. Structural weaknesses continue to impact the credit risk outlook of the sector. Those include tight lending conditions combined with high gearing of businesses, tight margins, uncertainty about the future spending capacity of public bodies, and the history of high levels of default frequency.

Related documents

1.06MB PDF