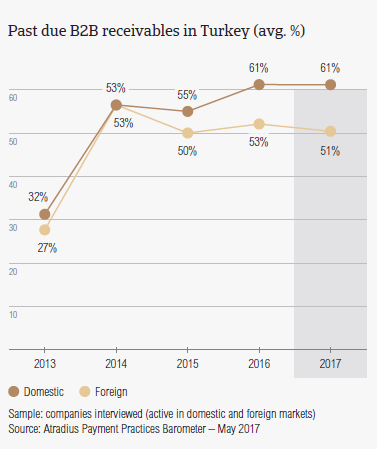

Compared to one year ago when 57.1% of B2B invoices were reported to be overdue in Turkey, the percentage has decreased slightly in 2017 to 55.9%.

Since 2015 increased political and economic uncertainty has negatively impacted Turkey’s business environment and the outlook for 2017 remains subdued. The difficult environment may have spurred Turkish respondents to increase protection against credit risk and sell more on credit terms than their peers in other Eastern European countries surveyed.

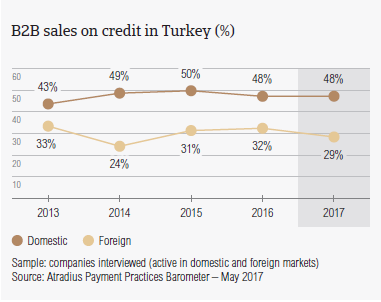

Sales on credit terms

In 2017, there has been a decrease in the percentage of the total value of B2B sales on credit in Turkey. However, with 38.1% of the total value of B2B sales made on credit, Turkey remains one of the Eastern European countries most inclined to use this payment method.

- 47.7% of the sales to B2B domestic customers was transacted on credit. This shows a minor decrease from 48.1% registered in 2016.

- The percentage of B2B sales on credit to foreign customers showed a more significant decrease from 32.4% last year to 28.5% in 2017. Together with respondents in Poland, Turkish respondents are some of the least inclined to offer credit terms to foreign B2B customers.

- Compared to the averages for Eastern Europe overall (domestic: 42.7%; foreign: 37.9%), respondents in Turkey are more open to granting credit terms to their domestic B2B customers. However, they are more averse to selling on credit to foreign B2B customers.

Overdue B2B invoices (%)

Compared to one year ago (57.1%), the percentage of overdue B2B invoices decreased slightly in 2017 (55.9%). However, the 2017 payment default rate recorded in the country is significantly above the average for Eastern Europe (41.5%).

- 89.3% of respondents in Turkey reported having experienced late payments from their B2B customers over the past year. This frequency of late payment is higher than that reported by respondents in Eastern Europe overall (83.7%).

- On average, 55.9% of domestic and foreign B2B invoices remained unpaid at the due date. Turkey has the highest percentage of overdue B2B invoices in Eastern Europe and the percentage of overdue invoices is also significantly higher than at regional level (42.9%).

- The Days Sales Outstanding (DSO) figure in Turkey increased from 63 days in 2016 to 73 days this year. In 2017, the difference between the country’s DSO and the regional average DSO (61 days) is of almost two weeks.

- Looking ahead, 34.8% of Turkish respondents do not expect a change in their annual DSO. However, 26.3% expect a slight increase and 24.9% a slight decrease. The small differences between these percentages point once more to a business environment dominated by uncertainty.

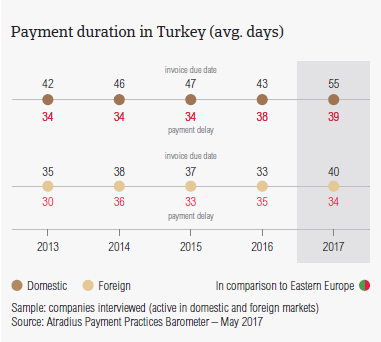

Payment duration (average days)

In 2017, domestic and foreign B2B customers of respondents in Turkey enjoyed the most relaxed payment terms in Eastern Europe. Despite this advantage, they generated some of the longest payment delays.

- Domestic B2B customers of respondents in Turkey were asked to settle their invoices, on average, within 55 days after the invoice date. This means that compared to domestic B2B customers in other Eastern European countries surveyed, they had 20 days extra to fulfil their payment obligations.

- Foreign B2B customers of respondents in Turkey were asked to settle their invoices within 39 days, on average. This is also four days longer than the average for Eastern Europe.

- Even with the longest average payment terms in the region, domestic B2B customers of respondents in Turkey delayed payments, on average by 40 days (38 days last year). In contrast, foreign B2B customers delayed their payments by an average of 34 days (2016: 35 days).

- This means it currently takes Turkish respondents 42 days from invoicing to turn overdue B2B invoices into cash. This is significantly longer than in the rest of Eastern European countries surveyed and almost 14 days longer than the average for Eastern Europe overall (29 days).

Key payment delay factors

According to respondents in Turkey, the main payment delay factor by domestic B2B customers remains liquidity constraints (cited by 58.0% respondents). In respect to foreign B2B customers, a staggering percentage of Turkish respondents (43.9%) pointed to the inefficiencies of the banking system.

- Similar to their peers in Eastern Europe, Turkish respondents indicated that the main reasons for payment delays by domestic B2B customers are insufficient availability of funds (58.0%), buyers’ intentional use of outstanding invoices as a form of financing (28.7%) and the formal insolvency of the buyer (23.6%).

- Looking at reasons for payment delays by foreign B2B customers, Turkish respondents mentioned the inefficiencies of the banking system (43.9%, the percentage is twice as high as in Eastern Europe overall), liquidity issues (35.8%) and the complexity of the payment procedure (34.1%).

- Over the past 12 months, overdue invoices caused 29.3% of respondents in Turkey to lose revenue. This percentage is significantly higher than in all of the other Eastern European countries surveyed.

- Late payments caused, 39.2% of respondents in Turkey to postpone payments to their own suppliers while 41.4% stated they needed to take specific measures to correct cash flow.

Protection of business profitability

Among the Eastern European countries surveyed, respondents in Turkey seem to be the most inclined to increase their use of credit management tools to protect themselves from risks arising from developments like Brexit, the slowdown in Asia and US protectionism.

- With 34.6%, Turkey had the lowest percentage of respondents who stated that they will maintain their current mix of credit management tool. At the same time, the country registered the highest percentage of respondents (26.9%) who intend to do more to protect their businesses from the negative impact of Brexit, the slowdown in Asia and US protectionism.

- Differently than in the rest of the Eastern European countries surveyed, where the most likely actions to be taken to improve credit management are checks on buyers’ creditworthiness followed by monitoring buyers’ credit risk, Turkish respondents seem more likely to improve their monitoring of buyers’ credit risk (33.4%) and increase bad debt reserves (30.0%).

- The impact of Brexit and that of the slowdown in Asia seem to prompt more Turkish respondents to increase protection and use more credit management techniques. Again, the two most likely actions to be taken are monitoring buyers’ credit risk (Brexit: 34.4%; slowdown in Asia: 35.3%) and increasing bad debt reserves (Brexit: 31.6%; slowdown in Asia: 31.4%).

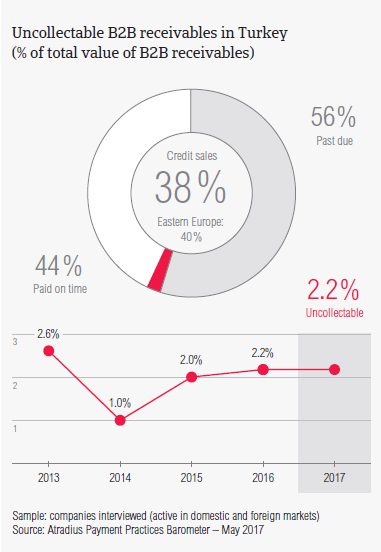

Uncollectable receivables

Turkey has the highest percentage of the total value of B2B receivables written off as uncollectable (2.2%) of the Eastern European countries surveyed. This is also more than twice the regional average (1.0%).

- The proportion of uncollectable B2B receivables in Turkey remained stable compared to last year (2.2%).

- Similarly to what was observed in previous surveys, uncollectable receivables in Turkey consisted almost entirely of domestic write-offs (domestic: 1.8%; foreign: 0.4%).

- In 2017, the largest proportion of uncollectable receivables came from the construction, consumer durables, textiles and services sectors.

- The main reasons why B2B receivables were uncollectable were the customers’ bankruptcy (53.8%), failure of collection attempts (46.2%) and the old age of the debt (24.7%).

Payment practices by industry

50.0% of respondents surveyed in Turkey expect an overall deterioration in the payment behaviour of their B2B customers over the coming 12 months. This is significantly more than the percentage of respondents stating this at regional level (26.0%).

- B2B customers of Turkish respondents in consumer durables (75 days), metals (73 days) and agriculture industry (63 days) enjoyed payment terms longer than the country average (47 days).

- In contrast, B2B customers originating from the electronics sector (35 days) were given shorter average terms to fulfil their payment obligations.

- Turkish respondents reported that customers from the construction industry and the consumer durables sector took the longest to settle payments (55 days and 54 days respectively).

- The main reason for the delay was insufficient availability of funds stated by 57.0% of respondents in the construction industry and by 47.0% in the consumer durables sector.

- Other key payment delay factors cited by suppliers in the construction industry were the buyers’ use of invoices as a form of financing (31.0%) and the complexity of the payment procedure (29.0%). Respondents in the consumer durables sector indicated other delay factors such as incorrect information on invoice (28.0%), disputes over the quality of goods and services provided and the formal insolvency of the buyer (both with 25%).