Financial conditions in Turkey will be tighter in the coming months.

This, together with higher inflation and a weaker exchange rate, will hamper domestic demand and probably lead to a sharp decrease in GDP growth in 2019. Turkish business insolvencies remain on an elevated level, with 80% of newly established businesses failing in the first three years. It is expected that business insolvencies will increase this year, especially in the property, construction and energy sectors. That said, it must be also underlined that even in industries severely affected by the current situation there are still many strong and resilient companies.

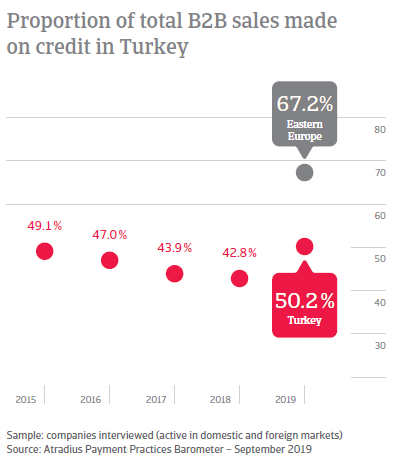

Modest increase in use of trade credit in Turkey reflects weak domestic demand and reduced competitiveness of exporters

The proportion of credit sales to B2B customers by Turkish survey respondents increased to 50.2% from 42.8% last year. This increase is the smallest of the countries surveyed in Eastern Europe. This might be a reflection of the sharpest decline in domestic demand since the second half of last year. It may also be connected to reduced dynamic export flows due to limited competitiveness in foreign markets, which in turn is caused by the high inflation rate and the volatility of the Turkish currency. As a result, in some major industries such as the construction and energy sectors, payment behaviour has already deteriorated, with extended payment terms and an increased number of payment delays.

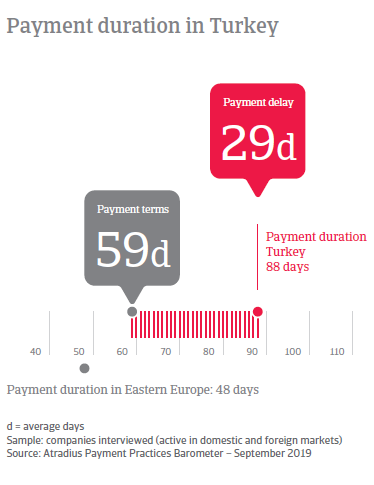

B2B customers of Turkish respondents enjoy the most relaxed credit periods in Eastern Europe

In such a challenging business environment, Turkish suppliers are attempting to stimulate sales growth by giving their B2B customers longer to settle invoices than last year. Average payment terms recorded in Turkey stand at 59 days from invoicing (up from 50 days last year). These are the longest observed in Eastern Europe and compare to a 37 days average for the region.

Turkish respondents are far more inclined to request payment on cash from B2B customers than their peers in Eastern Europe

Consistent with the bleak credit risk outlook for Turkey, far more respondents in Turkey (44%) request payment on cash from B2B customers, than in Eastern Europe (32%). In contrast, fewer respondents in Turkey (32%) than in Eastern Europe (39%) assess the prospective buyer’s creditworthiness prior to any trade credit decision. This may explain why far more respondents in Turkey (33%) than in Eastern Europe (22%) reserve against bad debts to ensure financial stability of the business should the assessment of the buyer’s creditworthiness prove inaccurate. A standout finding is that more respondents in Turkey (26%) than in Eastern Europe (18%) offer discounts for early settlement of B2B invoices, thereby avoiding the financing costs arising from the granting of trade credit.

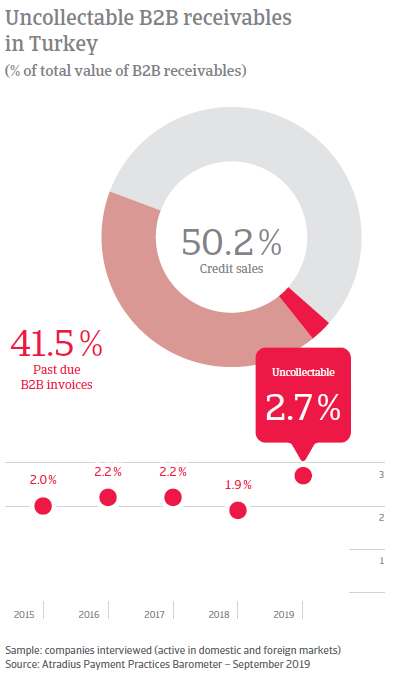

Turkey records the highest level of business insolvencies in Eastern Europe

41.5% of the total value of B2B invoices issued by Turkish respondents over the past year was past due. This is the highest figure recorded in Eastern Europe. In line with improved payment behaviour from customers, resulting in increased timely payments (53.1% of invoices paid on time compared to 40.3% one year ago), respondents in Turkey turn overdue invoices into cash significantly earlier than last year (87 days down from 92 days last year). However, to manage potential liquidity issues arising from late payments, 42% of Turkish respondents needed to delay payment to their own suppliers. 35% of respondents requested a bank overdraft extension, while 33% either pursued additional financing from external sources or took measures to correct cash shortfalls. A standout survey finding in Turkey is the marked increase in the proportion of write-offs of uncollectible accounts, currently averaging 2.7% of the total value of B2B receivables (up from 1.9% last year). This is the highest figure across all the countries surveyed in Eastern Europe and compares to a 1.6% regional average. This finding points to inefficiencies in collection of overdue accounts, ultimately eroding business profitability.

Turkish respondents are much more worried about a deterioration of their customers’ payment practices than their peers in Eastern Europe

Fewer respondents in Turkey (21%) than in Eastern Europe (60%) believe their B2B customers’ payment practices will not change over the coming months. In particular, Turkish respondents expecting customers’ payment practices to improve are far fewer (31%) than those expecting a deterioration (48%) ultimately leading to more receivables being written off as uncollectable. Amid concerns over tighter financial conditions in the coming months, 66% of Turkish respondents said that difficult access to bank financing would cause them to reduce their workforce and delay business investment due to lack of capital.

Overview of payment practices in Turkey

By business sector

B2B customers in the Turkish consumer durables sectors are given the longest payment terms

Turkish respondents from the consumer durables sector extended the longest payment terms to their B2B customers (averaging 73 days from invoicing). Average payment terms across the other sectors surveyed in Turkey range from 63 days in the construction sector to 52 days in the services sector. Respondents in the Turkish agri-food sector granted the shortest average payment terms to their B2B customers (49 days).

Trade credit risk is highest in the Turkish agri-food sector

Over the past year, trade credit risk in Turkey has significantly deteriorated in the agri-food sector, where over half of the total value of invoices remained unpaid at the due date. The services sector recorded the greatest improvement in customers’ payment speed over the past year. There was no change in the credit risk trend in the machines sector over the same period. However, as mentioned earlier, business insolvencies are expected to increase this year, especially in the property, construction and energy sectors.

Proportion of uncollectable receivables is highest in the machines sector

The ICT/electronics, agri-food and chemicals sectors in Turkey recorded the highest proportion of B2B receivables written off as uncollectable (3.5%, 3.2% and 3.1% respectively). At the lower end of the scale, the services sector recorded an average of 2.1% of receivables written off as uncollectable.

By business size

Large enterprises granted the longest average payment terms for B2B customers

Respondents from large enterprises in Turkey extended the longest payment terms to B2B customers. In contrast, micro enterprises offered the shortest average payment terms to B2B customers (averaging 68 days and 55 days from the invoice date, respectively).

Turkish micro enterprises and SMEs are the swiftest to cash in overdue invoices

Over the past year, both micro enterprises and SMEs in Turkey recorded the highest increase in the proportion of B2B invoices paid on time (+14% on average). Because of this improvement, both Turkish micro enterprises and SMEs are now the swiftest to collect payment of past due invoices (on average with 86 days from invoicing). Despite this, an average of 41% of the total value of B2B invoices issued by micro enterprises and SMEs in Turkey is past due. In contrast, it takes large enterprises on average 85 days from invoicing to cash in overdue invoices, (up from 71 day last year).

Large enterprises in Turkey recorded the highest rate of uncollectable receivables

Due to the significant lengthening of their invoice to cash turnaround process, Turkish large enterprises have a markedly worse track record when it comes to collecting overdue payments, with 3.1% of B2B invoices written off as uncollectable. The average for both SMEs and micro enterprises is 2.7%.