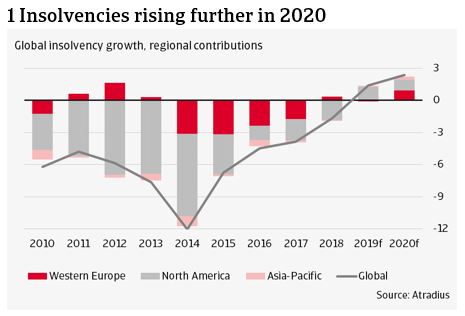

Corporate insolvencies are expected to grow 2.4% in 2020, a pronounced acceleration from the 1.4% increase recorded in 2019, largely resulting from the coronavirus outbreak

The outbreak of the coronavirus though is compounding the challenges to global trade and manufacturing, by weakening Chinese imports and tourism and causing disruption to global supply chains. The already-struggling global automotive sector is the most vulnerable industry to these disruptions. The mounting challenges have caused a downward revision of GDP growth forecasts around the world, especially in Asia, but also in Europe while less so North America. We evaluate that this downward revision in GDP growth translates into a worse insolvency outlook than the one from last quarter.

Negative global trade environment creating headwinds for European businesses

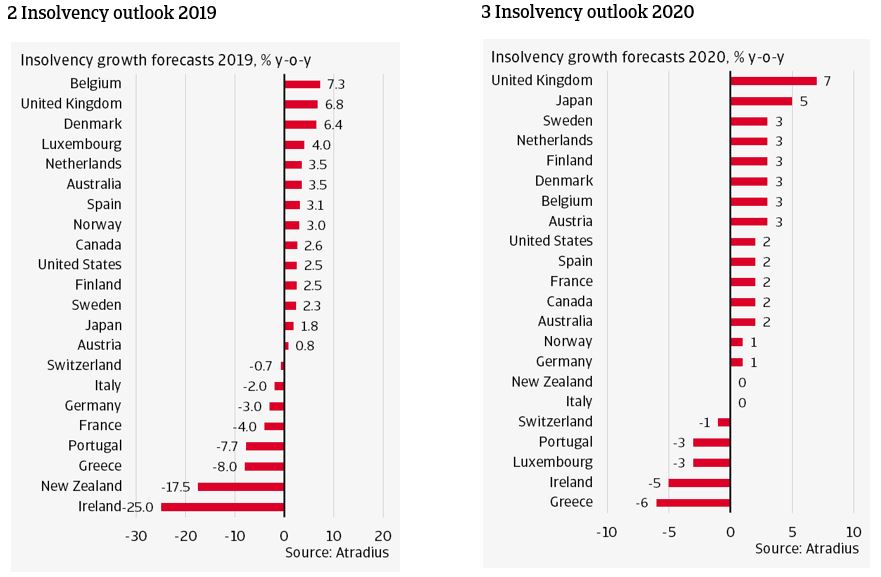

It is estimated that the number of Western European businesses going bankrupt will rise 2.1% in 2020, up from a 0.2% decrease in 2019. Global uncertainties and protectionist trade policies have been key drivers of the upswing. These factors are compounded by the coronavirus, which together pose a negative risk to financial stability and corporate solvency in 2020.

The United Kingdom is facing another year-on-year 7% increase in corporate failures, the highest rate in Western Europe. The Conservative Party’s landslide election victory in December 2019 and the following orderly departure from the EU in January 2020 have reduced short-term uncertainty but there are still significant hurdles for businesses in 2020. The economy stagnated in Q4 of 2019 and companies are facing subdued domestic and external demand. Uncertainty will increase, especially later this year as the exit from the customs union approaches. Business sentiment is set to decline in the face of rising trade barriers and the prolongation of uncertainty under trade negotiations with the EU will keep business investment pent up, especially weighing on SMEs down the supply chain.

Sweden and Denmark are also contributing to the region’s upward trend. In Sweden, insolvencies are forecast to increase 3% in 2020 as a result of persistent low GDP growth (1%). This weakness in is due to low external demand, an only modest recovery after the recent housing market downturn and signs of a loosening labour market. Insolvency statistics in Denmark display significant volatility due to statistical revisions and the relationship with economic performance is sometimes weaker than in other countries. With this in mind, we forecast insolvencies to increase 3%. Economic growth is slowing in 2020. Moreover, supply chain disruptions and weaker global trade caused by the coronavirus outbreak represent headwinds for Denmark’s exporters and importers early this year.

In Switzerland 2019 marked a turning point for insolvencies after years of increases following the scrapping of the Swiss franc’s (CHF) ceiling against the euro. This positive momentum is likely to continue in 2020 with GDP growth accelerating between 0.3 and 0.5 percentage points higher than in 2019 as international sporting events boost service exports. Growth is also underpinned by continued strong performance of the labour market. Downside risks – especially external demand and capacity constraints – continue to surround the Swiss economy. Global trade uncertainty has increased demand for the Swiss franc, a safe haven currency. CHF appreciation particularly challenges the hospitality sector, which is facing the second highest insolvency number after construction. Swiss exporters are also negatively affected, as exports comprise two-thirds of Swiss GDP.

GDP growth in the eurozone is expected to weaken to 0.8% in 2020, compared to 1.2% in 2019. This slowdown reflects the prevailing weakness in manufacturing combined with the impact of the coronavirus on supply chains across the world. According to the Q4 2019 ECB bank lending survey, credit standards for loans to businesses remained largely unchanged. With economic growth subdued and inflation expectations muted, the ECB will keep interest rates at their current historically low levels with an eye to further cuts if needed. Credit standards are therefore likely to remain accommodative, containing aggregate insolvency growth to 1.1%.

In Germany, the manufacturing sector is showing signs of stabilisation, but weak external demand and elevated uncertainty continue to take their toll on German industry. Domestic demand remains solid, supported by a healthy labour market and expansionary fiscal policy. However, growth is expected to remain weak in 2020 as the international trade slowdown remains a headwind for German exporters. US-China trade tensions continue to weigh on prospects of the German automotive sector. While German business failures are expected to increase only 1% in 2020, this increase marks a turning point after a decade of declining annual insolvencies.

As small, open economies, Belgium and the Netherlands face moderating growth in 2020, caused by headwinds from weak global trade and high levels of uncertainty. External headwinds are weighing on exports and business investment, despite supportive financing conditions. However, domestic demand remains robust, driven by a tighter labour market and accelerating wage growth. In Belgium, however, monthly employment growth is now showing signs of slowing, as firms turn more cautious on hiring.

After several years of annual decreases, 2019 marked a turning point for insolvency growth in both the Netherlands and Belgium. Dutch insolvencies rose by 3.5% in 2019, likely followed by another 3% increase this year. Belgian bankruptcies rose by 7.3% in 2019, partly because of a revision of bankruptcy law. This year is likely to bring another rise of 3% in Belgian insolvencies as economic growth slows.

The UK is a major trading partner for the Netherlands and Belgium. While the chance of a no-deal Brexit has reduced after the withdrawal agreement between the UK and the EU, it is not completely off the table – posing a downside risk particularly for the machinery and chemicals sectors.

In France, weaker external demand is expected to weigh on economic activity as well, further compounded by the outbreak of the coronavirus. The outlook is more optimistic regarding domestic demand, as household purchasing power will continue to benefit from fiscal support, low inflation and rising wages. Employment growth is likely to moderate, but remain robust, notably in the private sector, keeping the unemployment rate on a downward trend. Although investment is set to cool down, it should remain more dynamic than economic activity in general. The number of insolvencies is still forecast to increase 2% in 2020 on lower economic activity, following a 4.0% decline in 2019.

Domestic demand will remain the main driver of growth in Spain, however that growth will be at a slower pace than in recent years, with moderating employment growth weighing on consumption and heightened uncertainty hindering investment. Growth is expected to cool in 2020 following several years of robust recovery. Business failures are expected to increase 2% in 2020, after they rose 3% in 2019. While the level of insolvencies remains five times higher than before the crisis, it is no longer on a declining trend. The Spanish economy has reached a new normal when it comes to bankruptcies, and a further decline is no longer self-evident.

The Portuguese economy has seen a swift recovery in recent years, translating into a declining insolvency level. A 3% decline in insolvencies is expected in 2020, following a 7.7% decline in 2019.

In Italy, we forecast a stagnation of business failures in 2020 as the economy is coming to a standstill. GDP contracted 0.3% q-o-q in Q4 of 2019, the worst performance since early 2013, mainly due to subdued domestic demand. The most recent indicators suggest that the stagnation in industry is not over yet, and the sudden outbreak of coronavirus in the country spells further challenges for business activity – disrupting travel and supply chains, diminishing consumer and business sentiment, and declining tourist inflows. The insolvency outlook is subject to high political uncertainty, as tensions rise within the fragile governing coalition and may further increase between the Italian government and the European Commission, potentially weighing on sentiment and financing conditions for the private sector.

Ireland experienced a sharp 25% decline in business failures in 2019, the third year in a row of double-digit decreases fuelled by strong domestic demand, bringing the number of annual insolvencies closer to its pre-crisis level. The outlook for 2020 is weaker and we expect to see a bottoming out of the downward trend during the year, but given base effects from 2019, we still forecast a 5% decline. GDP growth is likely to recede to lower territory in 2020 as demand from key export markets (UK and US) is declining, while the domestic economy faces increasing capacity constraints and lower government spending. The downside risk of a no-deal Brexit has diminished, providing a stimulus for consumer confidence but domestic political uncertainty has increased following inconclusive elections in February 2020. The coronavirus outbreak poses a downside risk to Irish businesses as a small, open economy, especially for its tech sector, which is dependent on Asian supply chains.

North America: business failures still rising but at a slowing pace

The upward trend in US business insolvencies appears to have peaked in Q3 of 2019, bringing full year growth to 2.5%. We expect this upward trend to gradually moderate, bringing 2020 insolvency growth to 2%. Corporate bankruptcy filings have increased in the agricultural sector, which was particularly targeted by Chinese tariffs. The retail sector is grappling with higher import costs as a result of the trade war, as well as higher labour costs and high price competition. While still challenging, the business environment is more benign than last year given the tentative progress in trade talks with Beijing. General uncertainty should be further mitigated by the end to the impeachment trial and the upcoming elections which will most likely deter major changes in policymaking. The dovish stance of the Federal Reserve is further cushioning the business environment, but weaker domestic energy activity due to low oil prices and a strong USD will continue to strain business investment.

Canadian business failures are following a similar trend as in the US. After spiking in mid-2019, the annual increase in insolvencies moderated to 2.6% for the full year. We expect this to moderate further to 2% in 2020 as the economy bottoms out. Lower oil investment, weak consumer spending and high uncertainty will continue to weigh on business activity. But the Bank of Canada is likely to cut interest rates another 50 basis points and uncertainty should ease, both helping the business environment. As Canada depends on the US for trade, the new USMCA agreement should alleviate uncertainty for businesses, following its expected ratification by Canada. Relations with its southern neighbour will likely remain strained though.

Asia-Pacific: spill-overs from China increase rate of insolvency growth

Compared to other regions, Asia-Pacific faces the highest increase in insolvencies in 2020 (+4.2%), in part due to its close ties to China. The coronavirus outbreak will strain the recovery in the ICT sector, which is a major Asian supply chain. Japan, a key manufacturer of high-tech components for this chain, is facing a 5% rise in insolvencies this year. Supply chain disruptions and lower Chinese demand for imports will stifle the nascent recovery in Japan’s ICT sector, boding ill for Japan’s fragile economy. On top of sluggish exports, the consumption tax hike, labour shortages, and a series of natural disasters caused the economy to contract 1.6% q-o-q in Q4 of 2019 (6.3% annualised) and marked the first year of increasing corporate bankruptcies (+1.8%) in 11 years. The economic challenges are expected to continue to constrain GDP growth this year, halving economic growth to 0.5%. Retail and transportation are especially hard hit by the consumption tax increase and corporate solvency will be further challenged by reduced Chinese tourism.

Australia’s economic outlook is also negatively affected by the coronavirus outbreak. The downturn in East Asia is expected to adversely affect the export services sector in Q1 of 2020 through a lower turnover in tourism. Moreover, negative spill-over effects on other sectors are likely to persist this year due to lower demand from Chinese consumers. The coronavirus has also affected commodity prices through lower Chinese demand, which have already been under pressure due to the lower global industrial activity. Overall, we believe that a continuation of a modest GDP growth will keep insolvencies increasing at 2% in 2020.

Dana Bodnar, economist

dana.bodnar@atradius.com

+31 20 553 3165

Theo Smid, economist

theo.smid@atradius.com

+31 20 553 2169