Increased credit risk for highly leveraged automotive suppliers

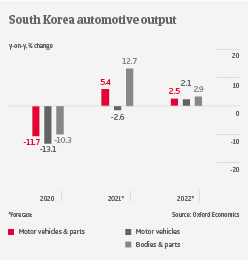

After contracting 11.7% in 2020, South Korean automotive output is forecast to rebound by about 5% in 2021 and 2.5% 2022. New car sales increased year-on-year in H1 of 2021 in the domestic market and abroad, but have started to decrease since then, as semiconductor shortages have caused supply and production disruptions. Lower output by large South Korean Original Equipment Manufacturers (OEMs) has a ripple effect along the value chain. While the profit margins of OEMs have remain stable so far, those of suppliers have started to deteriorate. At the same time, the financial situation of some Tier 2 & 3 suppliers is more strained due to larger borrowing.

Many Tier 1 suppliers are already preparing for the transition towards e-mobility, expanding related facilities. However, this transition will prove to be more difficult for Tier 2 & 3 businesses, which often lack the necessary financial strength and technological skills. While the South Korean government has not yet launched a support scheme for suppliers, it plans to spend USD 10.3 billion in 2022 for e-mobility, including incentives for hydrogen and battery-electric vehicles and charging stations.

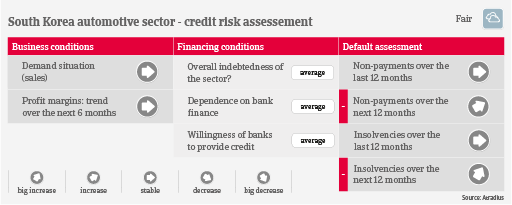

Payments in the automotive industry take about 60 days on average. Both payment delays and insolvencies are expected to increase in 2020, mainly affecting those smaller suppliers that already face financial difficulties (e.g. due to high leverage) and suffer most from production cuts, sales decrease, deteriorating margins and extended credit terms. Currently it is expected that business failures will increase by about 20% in the coming twelve months, but the rise could be even higher if the current supply issues last in H1 of 2022.

Our underwriting stance remains generally neutral for OEMs and Tier 1 suppliers, which are generally able to cope with deteriorating sales and margins, helped by their financial strength and strong group background. Due to the elevated credit risk of Tier 2 & 3 businesses, our underwriting stance is generally more restrictive for this segment.