Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

China

China

Australia

Australia

Austria

Austria

Belgium

Belgium

Bulgaria

Bulgaria

Canada

China

Canada

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Kingdom

United Kingdom

United States

United States

巴西

巴西

葡萄牙

葡萄牙

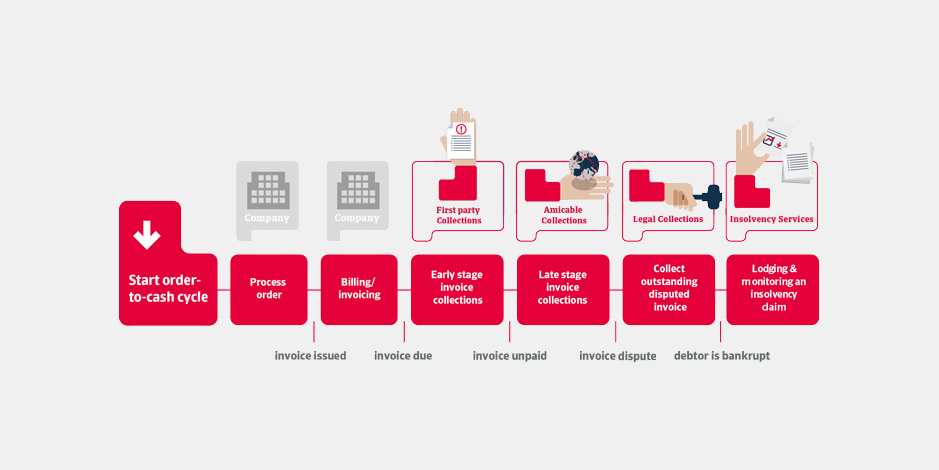

Our experienced debt collections team, Atradius Collections, are located throughout the world to support your collection of outstanding invoices in any country, time zone, currency and language.

As an Atradius customer, you’re automatically able to access and benefit from our debt collections service, Atradius Collections. This is a feature of all our Credit Insurance policies and will not incur any additional cost for you.

We also offer a standalone Atradius Collections service to organisations and business that are not Atradius Credit Insurance customers.

As debt collections specialists, we know how to respond to excuses for non-payment and exert the right level of pressure to maximise revenue collection.

We also know that a proactive and sensitive approach can often yield the best results. A payment plan for a customer experiencing cashflow problems may result in complete settlement of the debt and the retention of a strong working relationship with you. To that end, we work closely with you to seek the quickest and most appropriate solution for you.

"Atradius Collections supported us in a few cases when the relation with some customers became problematic."

As debt collections specialists, we’ve heard most of the excuses businesses make when they fail to pay a bill. We know how to respond to this and how to exert the right level of pressure to maximise revenue collection.

However, we also know that a proactive and sensitive approach can often yield the best results. For example, a payment plan for a customer experiencing cashflow problems may result in complete settlement of the debt and the retention of a strong working relationship with you. To that end, we work closely with you to seek the quickest and most appropriate solution for you.

With the benefit of our worldwide IT infrastructure, we operate the most integrated Collections network in the industry. Our fully automated approach allows us to act promptly upon receipt of a notification of non-payment, regardless of time zones.

If you’re an Atradius Credit Insurance policy-holder, you may manage Collections through Atradius Atrium.

Non-policy holders may also access our collections expertise on a case by case basis. As an Atradius Collections-only client, you may track your case through our dedicated system, Collect@Net.

Contact us